To: R-CALF USA Members, Affiliates, and All

From: Bill Bullard, CEO

Date: June 12, 2026

Subject: UPDATE: USTR Proposes Exempting Brazilian Beef from Proposed Tariffs on Brazil; Comments Requested

Background: We encourage all our members to submit comments on the Office of the U.S. Trade Representative’s (USTR’s) proposal to exempt all imports of Brazilian beef from the 25% tariff that USTR plans to apply to most all other goods of Brazil.

As promised, below are the draft comments that R-CALF USA plans to submit. These are Draft comments and numerous reference citations will be included, along with minor changes before it is finalized and submitted.

Meanwhile, please use any part of these comments to formulate your own. Your comments can be very brief or extensive, whichever you prefer.

The important point is that the USTR receives a resounding message from America’s cattle producers that the ongoing importation of beef from Brazil is harming the U.S. cattle industry and the U.S. cattle industry supports stopping the illegal deforestation in Brazil.

Action: Here’s how to submit your comments on or before July 1, 2026, to express opposition to the USTR’s plan to exempt Brazilian beef from the proposed 25% tariff on other Brazilian goods.

You can submit your comments through the online USTR portal at: https://comments.ustr.gov/s/. The docket number for comments is USTR-2026-0331.

You can review the entire notice, including the opportunity to appear at the USTR hearing here: Federal Register :: Notice of Determination and Request for Comments Concerning Action Pursuant to Section 301: Brazil’s Acts, Policies, and Practices Related to Digital Trade and Electronic Payment Services; Unfair, Preferential Tariffs; Anti-Corruption Enforcement; Intellectual Property Protection; Ethanol Market Access; and Illegal Deforestation

Here are R-CALF USA’s Draft Comments:

Dear Sir or Madam:

R-CALF USA is a national, non-profit association representing approximately 4,000 independent U.S. cattle farmers and ranchers and sheep producers in 42 states. It is the largest U.S. producer-only trade association representing the U.S. cattle industry. R-CALF USA works to sustain the profitability and viability of the U.S. cattle and sheep producers, whose farming and ranching businesses are vital to America’s rural economy. R-CALF USA’s membership consists of independent cow-calf operators, cattle backgrounders and stockers, cattle and sheep feedlot owners, and sheep producers. Various main street businesses are associate members of R-CALF USA.

R-CALF USA agrees with the United States Trade Representative’s (Trade Representative’s) determination that certain of Brazil’s acts, policies, and practices at issue in the above captioned investigation are actionable under Section 301(b) and Section 304(a) of the Trade Act of 1974, as amended (Trade Act). R-CALF USA further agrees that the Trade Representative’s proposed determination that action is appropriate and that appropriate action would include applying tariffs of 25% on all goods of Brazil, with exemptions for certain goods, is generally appropriate; but with the critically important exception that beef products identified in the Annex should not be exempted from the tariff application.[1] Moreover, trade data reveal that though Brazil has far exceeded its applicable tariff rate quota, the requisite 26.4% over quota tariff rate is inadequate to deter what are now record Brazilian beef imports, an indication that the appropriate tariff rate for Brazilian beef should be considerably higher than the 25% rate currently proposed by the Trade Representative for non-exempted goods from Brazil.

1. Tariffs on Brazilian Beef Are Needed to Reduce or Eliminate Illegal Deforestation in Brazil

The Trade Representative’s investigation expressly identified a direct nexus between Brazilian ranching, cattle, and beef and illegal deforestation, with respect to which Brazil’s acts, policies, and practices were found to be unreasonable and burden or restrict U.S. commerce and, therefore, actionable. Citing a 2024 study, the investigation determined that Brazil’s policies failed to adequately prevent illegal ranching, and deforestation.[2] The investigation further implicated Brazilian cattle ranching as a primary impetus for deforestation, citing the conversion of forest to pastureland for cattle as the initial stage of the deforestation process, and citing Brazilian cattle ranchers’ desire to continue expanding production as further motivation to cut down more primary forest as the deforestation process’s final stage.[3]

Indeed, the investigation cited the estimate that since 2001, over 90% of Brazil’s deforestation (legal and illegal) is attributable to the conversion of primary forest to agricultural production, and “between 2018 and 2022, cattle ranching drove 78% of commodity-attributed deforestation.”[4]

The investigation proceeds by explaining that without effective enforcement of environmental laws, Brazilian ranchers may launder cattle raised illegally on deforested land by transferring them to legitimate slaughterhouses. Compounding this illicit cattle laundering vector is the Trade Representative’s knowledge that Brazilian ranchers are known to bribe government officials to hide their illicit deforestation-related activities.[5]

Upon the establishment of such a direct and prominent, if not the primary link between Brazilian cattle ranching and Brazil’s illegal deforestation, exempting the principal derivative of cattle, i.e., beef, from the proposed 25% tariff action would substantively undermine the Trade Representative’s objective of eliminating the improper acts, policies, or practices contributing to illegal deforestation in Brazil.

2. Brazilian Beef Products Should Be Removed from the Annex’s List of Exemptions

Presumptively, the Trade Representative understands that Brazilian cattle ranching is a primary catalyst, if not the primary catalyst, driving illegal deforestation in Brazil. However, it appears he has decided to forego the remedial effect the proposed tariff action would have on Brazil based on a belief that Brazilian beef meets one or more of the conditional criteria for exemption listed in the proposed action’s Annex.

With respect to beef, the last of the four conditional criteria for exemption addresses the efficacy of tariffs to encourage Brazil to reduce or eliminate illegal deforestation. The presumptive operating theory underpinning the proposal to apply tariffs on other Brazilian goods is that tariffs would frustrate Brazil’s economic objectives, causing it to change its specific acts, policies, and practices that led to the tariff’s imposition. There is nothing peculiar about beef – the derivative of cattle and, therefore, the catalyst of illegal deforestation – to suggest that beef tariffs would not frustrate Brazil’s beef export objectives any more or less than tariffs on all the other Brazilian goods contemplated under the proposal would frustrate Brazil’s other economic objectives and lead to the elimination of those act, policies, and practices the USTR found actionable. Indeed, exempting beef from the proposed 25% tariff would substantially thwart USTR’s efforts to reduce or eliminate Brazil’s illegal deforestation as well as some of USTR’s other actionable findings, including USTR’s finding that Brazil maintains unfair, preferential tariffs and Brazil does not properly conduct anti-corruption enforcement.

The first three conditional criteria relate to whether the United States is dependent on the Brazilian goods potentially subject to the proposed tariff, and whether tariffs on those goods would cause harm to the U.S. should the tariffs reduce or deprive the U.S. of those products. With respect to beef, and as demonstrated below, the U.S. economy is reeling from decades of failed trade policies that have facilitated excessive beef and cattle imports into the United States. These excessive imports have substantially displaced domestic beef production; substantially contributed to the long-term contraction of the U.S. cattle industry in terms of its participants, herd size, and marketing opportunities; substantially contributed to the disconnect between domestic cattle prices and retail beef prices (as evidenced by the recent, multi-year period when beef prices were reaching new highs and cattle prices were trending downward); substantially contributed to the hollowing out of Rural America; and substantially contributed to supply chain disruptions. In recent years, Brazilian beef imports have increased substantially, and those imports are playing an ever-increasing role in relegating the United States increasingly dependent on foreign countries for one of its most important protein sources – beef, which is antithetical to national security.

3. Not Delimiting the Ongoing Importation of Brazilian Beef Will Harm the United States

To demonstrate why it is wrong to presume that delimiting the ongoing importation of Brazilian beef would in any way be harmful to the United States – indeed, why the opposite is true, the role of beef and cattle imports – including Brazilian beef’s escalating role in recent years, in the decades-long contraction of the U.S. cattle industry’s beef cow inventory requires careful analysis.

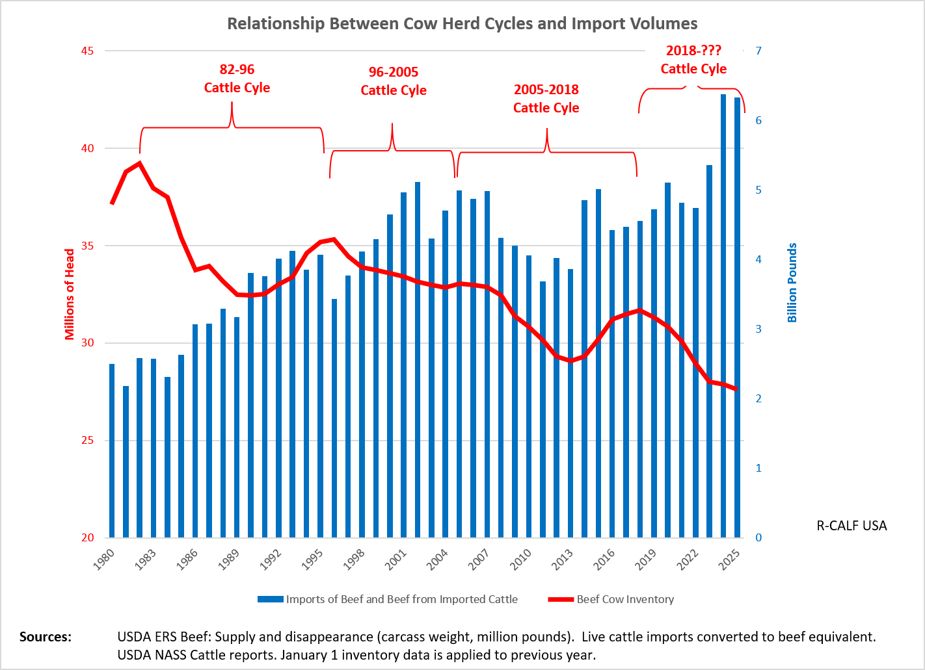

As shown in Chart 1 below, the U.S. beef cow inventory has trended downward since peaking in 1982, though there were several periods of expansions and liquidations during this overall downturn. Together, the periods of expansion and liquidation of the cow herd inventory are known as the cattle cycle, and each complete cycle is measured between each inventory peak. Historically, the cow herd inventory expands when cattle prices are favorable and liquidates when they are not. In essence, the cattle cycle is a historical phenomenon representing the industry’s collective adjustments to balance domestic cattle supplies with beef demand and it is influenced by the long biological cycle of cattle. Cattle price trends serve as a proxy for the relative balance between supply and demand. When prices trend upward, it signals to ranchers the need to expand the cow herd, and vice versa.

There were three complete cattle cycles between 1982 and 2018. The U.S. cow herd is presently in a prolonged liquidation phase within the current uncompleted cycle that has so far persisted for seven years since the latest peak in 2018. This liquidation phase, as well as each preceding liquidation phase depicted in the chart, is abnormal as the liquidation phase of the cattle cycle is typically expected to last only three to four years.

Because imported beef and cattle are direct product substitutes for domestic beef and cattle, changes in the volume of beef and cattle imports entering the U.S. influence domestic supply, which in turn influence domestic cattle prices and, hence, the cattle cycle. As Chart 1 shows, import volumes have more than doubled since 1980. The chart further shows that each liquidation phase of each cattle cycle since 1996 was clearly preceded by a marked increase in the volume of imports. Also evidenced by the chart is the fact that each successive inventory peak in each cattle cycle since 1982 was lower than the preceding cycle’s peak, resulting in a long-term, downward trending beef cow inventory that is now historically low – the smallest inventory since 1951. Unsurprisingly, the decreasing size of the U.S. beef cow herd that has reached historically low levels occurred contemporaneously with increasing imports that have now reached record high levels.

Chart 1

Chart 1 above reveals the U.S. beef cow herd was liquidating from 2005 through 2013, resulting in the smallest beef cow inventory in 70 years – approximately 4 million beef cows were liquidated from the herd between 2005 and 2013. However, responding to upward trending cattle prices leading up to 2013, cattle ranchers began expanding the beef cow herd in 2014. From 2014 through 2018, the U.S. beef cow herd regained ~3.6 million of the ~4 million beef cows that had been liquidated from 2005 through 2013. However, cattle prices were trending downward contemporaneous with the 2014 through 2018 herd expansion and after 2018, the beef cow herd succumbed again to lower prices and American ranchers resumed their cow herd liquidation.

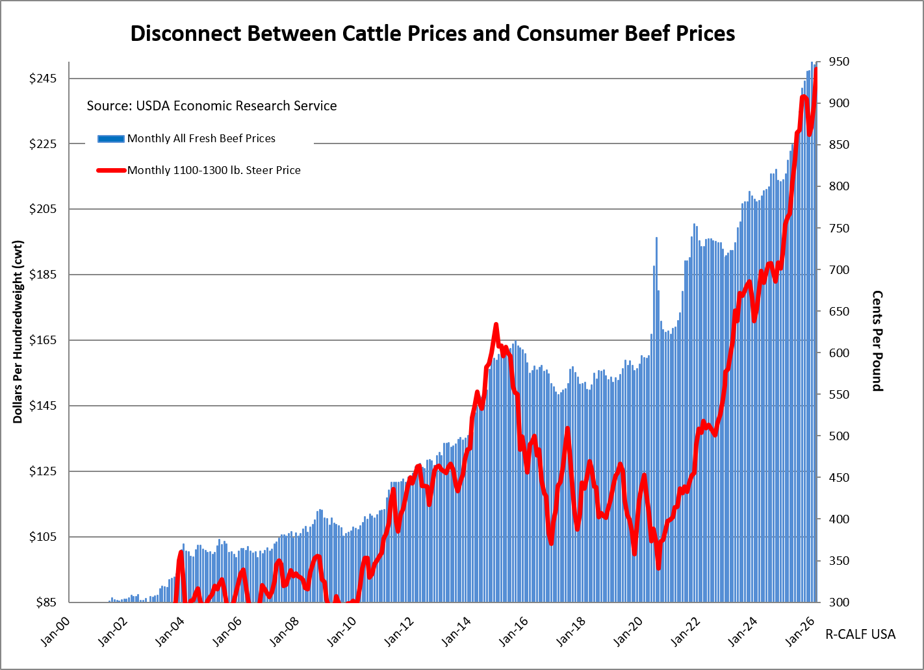

It is important to note that contrary to media reports indicating that drought caused the most recent downturn in the beef cow inventory, the latest liquidation phase of the U.S. beef cow herd began in 2018, which was well before the widespread drought that began around 2021. It was the ranchers’ response to downward trending cattle prices depicted in Chart 2 below that triggered the 2018 outset of the latest herd liquidation, while the drought occurring during the liquidation’s pendency merely exacerbated the herd’s ongoing decline.

Chart 2

Note particularly in Chart 2 the prolonged period between 2015 through 2022 when domestic cattle prices were trending downward and retail beef prices were inexplicably trending sharply upward. This inverse relationship between cattle prices and retail beef prices shown in Chart 2 and the inverse relationship between import volumes and the contraction of the U.S. beef cow inventory in Chart 1 together highlight the severe market failure in both America’s cattle markets and retail beef markets that is substantially harming the United States. Moreover, when the positive relationship between rising import volumes and rising retail beef prices is revealed by comparing the relevant data streams depicted in Charts 1 and 2 are considered, this further reveals market failure in the retail beef market and directly contradicts the notion that consumer affordability can be achieved by further increasing import volumes.

That rising imports have substantially contributed to the long-term and ongoing contraction of the U.S. beef cow inventory is manifest. The U.S. Department of Agriculture has long known that increased imports lower producer welfare by lowering domestic cattle prices, but it has long rationalized that such harm to the domestic cattle industry was justified by theoretical gains in consumer welfare, which the USDA believed resulted from lower beef prices and more choice for consumers. This theory cannot be squared with reality as rising import volumes since 2011 have corresponded with higher retail prices, which have become even more acute over the past three years, 2023-2025, when import volumes reached year-over-year record highs, as did retail beef prices.

The fatal flaw in USDA’s consumer welfare theory was the lack of understanding of the low margins that sustained America’s widely dispersed, family-scale ranching operations. The lower cattle prices associated with the modeled producer welfare losses caused a mass exodus of America’s beef cow operations (with over 50% of them exiting the industry since 1980) and a concurrent reduction in America’s beef cow inventory, ultimately leading to the extreme imbalance between cattle supplies and beef demand manifest today. The missing element in USDA’s theory was balance. The agency should have endeavored to manage import supplies at levels that would compliment domestic production, not displace it and its attendant domestic infrastructure as excessive imports continue to do.

4. Brazil’s Role in the Ongoing Contraction of the U.S. Cattle Industry and Dysfunction of U.S. Cattle and Beef Markets

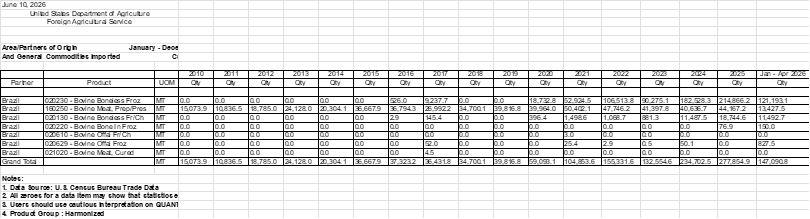

Trade data copied below in Chart 3 show that prior to 2016, the U.S. imported only processed (pre-cooked) beef (HTSUS 160250) and cured beef (HTSUS 021020) from Brazil, due to U.S.-imposed foot-and-mouth disease (FMD) restrictions. By 2016 the FMD restrictions were lifted, and in 2016 and 2017 the U.S. began additionally importing relatively small quantities of boneless frozen and boneless fresh and chilled beef and frozen offal from Brazil. However, because of repercussions from the Brazilian beef scandal that surfaced in 2017, the U.S. again ceased importation of all but processed beef from Brazil from 2017 through 2019.

Beginning in 2020, however, the importation of Brazilian fresh beef, processed beef, and cured beef increased dramatically, increasing 48% from 2019 to 2020 and 598% from 2019 to 2025. Total world imports increased 25% from 2019 to 2025, indicating that increased imports from Brazil were contributing substantially to the overall increase in imported beef in the U.S. market.

Chart 3

The herd expansion that began in 2014 was repelled by near record import volumes in 2014 and 2015, and steadily increasing imports from 2016 through 2020, the year Brazil began its grand reentry into the U.S. market with substantial volumes of fresh, chilled, and frozen beef, along with increased volumes of processed beef. In 2020 Brazil was the fifth largest source of U.S. beef imports. In 2025 it ranked third. During the first quarter of 2026, Brazil was the largest source of U.S. beef imports.

Importantly, since 1994, it has been U.S. policy to discourage over quota imports from Brazil and other countries that fall under the 65,005 metric ton TRQ category designated for “other countries.” This beef TRQ was intended to protect the domestic industry against excessive imports by applying a 26.4% tariff on beef imports that exceed the TRQ. Brazil, on its own, has blown past the entire 65,005 MT TRQ during each of the past four years, relegating the TRQ ineffectual at protecting the domestic industry and indicating that a 26.4% over-quota tariff on Brazilian beef is woefully insufficient to discourage excessive imports from Brazil.

The year-over-year increases in beef imports from Brazil measured since 2023 are all but certain to continue; and all but certain to continue discouraging American ranchers from investing in any measurable and enduring expansion of the diminished U.S. beef cow herd.

Allowing unrestrained beef imports from Brazil is contrary to USTR’s objective of eliminating illicit deforestation in Brazil. In fact, exempting beef from the USTR’s proposed tariff will likely lead to higher beef prices for Brazilian exporters, rewarding them for the illegal deforestation already commenced and incentivizing them to expand their illicit deforestation practices.

5. Conclusion

[To be added]

Sincerely,

R-CALF USA

[1] The Annex at 91 Fed. Reg., 33,862 – 33,863, identifies numerous beef products with HTSUS heading ranging from 0201.10.05 to 0210.20.00, which includes bovine carcasses, meat cuts, high-quality meat cuts, offal, tongues, and livers.

[2] See 91 Fed. Reg., at 33,858.

[3] See id.

[5] See id.

# # #

Ranchers Cattlemen Action Legal Fund United Stockgrowers of America (R-CALF USA) is the largest producer-only lobbying and trade association representing U.S. cattle producers. It is a national, nonprofit organization dedicated to ensuring the continued profitability and viability of the U.S. cattle and sheep industries. For more information, visit www.r-calfusa.com or call 406-252-2516.